Your Strategy Should Maximize Profits, Not Just Chase Revenue.

Most businesses are busy, but few are truly profitable. The key isn't working harder. It's implementing a smarter strategy to strengthen your bottom line. Let's pinpoint the high-impact opportunities you've been overlooking.

The Profit Strategy Your Competitors Don't Know

Watch this detailed video to learn the secret to exponential growth. I'll walk you through a simple but powerful strategy that you can implement in a single afternoon to gain an immediate and significant advantage in your market.

Learn a growth model unknown in your industry.

Get the complete framework for doubling your profits.

Start implementing these powerful changes today.

One-On-One Coaching

Looking for professional help that’s affordable? I will help you increase your leads and sales, generate leads, create marketing that actually produces results, increase your revenue substantially, and position your business as the dominant force in your industry.

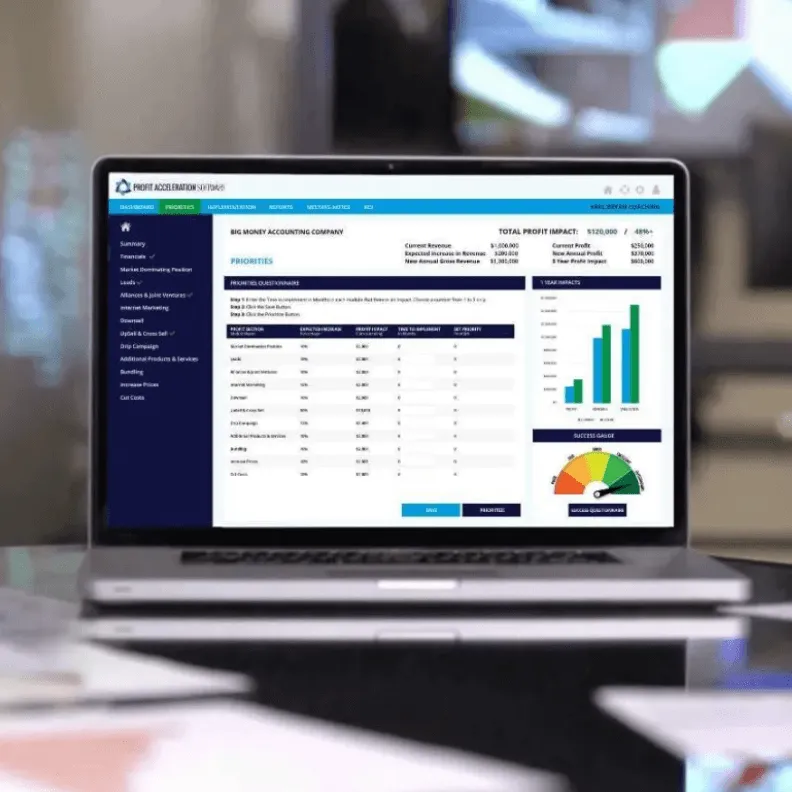

Profit Acceleration Simulator

Success is achieved through small, incremental changes in multiple areas of your business. We've defined 12 areas that generate immediate increases both revenue and profits, without spending a cent on marketing or advertising.

DIY Online Learning

Everything a Small Business Owner needs to know to improve profits. Includes access to all business spreadsheets, e-classes, internet marketing videos, sales letters, profitable headlines, proven marketing material strategies, articles, tips and much more!

Group Coaching

My group coaching program will allow you to not only learn new business growth strategies from me, but also other small business owners with the same goals as you have for your own business. We will work on application of these strategies because knowledge is pointless without using it.

Unleash Your

Business Profits.

Turn Your Vision into Reality with Expert Guidance.

Building Bridges to Your Business Dreams.

Inspire, Empower, Succeed.

Watch this complete training video on the power of Profit Acceleration.

Video may need update

Unleash Your Business Brilliance.

We will assess your business using our revolutionary new Profit Acceleration Software™. We will then detail the specific strategies that can generate massive financial breakthroughs for your business.

At the end of our session I will send you your own customized roadmap for success along with a detailed report that will position your business as the dominant force in your industry.

A clear plan removes the guesswork, paving the way for sustainable success.

Your Blueprint for Profitable Growth.

Unleash Your Business Profits.

It's time to stop guessing and start growing with a clear, strategic plan. We'll guide you through a proprietary assessment of your business to identify the most significant financial breakthroughs you're currently overlooking.

At the end of our session, you will receive a customized roadmap for success—a detailed report that positions your business as the dominant force in your industry.

Guiding You to Profitable Possibilities.

Guidance that provides the clarity needed to navigate your next steps with confidence.

Strategic One On One Coaching.

It's time to move forward with intention. We'll work together to analyze your current business landscape, uncovering key areas for development and refinement that you may not have seen. Our collaborative process is designed to bring focus and direction to your long-term objectives.

You will emerge from our session with a clear understanding of your next steps and the strategic insights required to confidently propel your business forward.

Guiding You to Profitable Possibilities.

Business Greatness Through Community.

Empowering Business Owners to Thrive.

Invest in Your Business, Invest in Your Success.

New Book From Terry Massey

Discover how to unlock more profit from your business. This free guide provides a step-by-step roadmap to greater profitability. Download your copy instantly.

Find new revenue without new ad spend

Convert more prospects into customers

Simple methods to increase your margins

Testimonials

Driving Growth, Amplifying Impact

Unleash Your Business Profits.

I guide serious business owners and organizations in focusing on the key activities and systems that support growth in clients, sales, and profits.

Ready To Get Started?

Email:

Phone Number:

Trusted By

Copyright © 2026 AmeriStride. All rights reserved

DISCLAIMER

The information contained on this website and the resources available for download through this website is not intended as, and shall not be understood or construed as, professional advice. While the employees and/or owners of the Company are professionals and the information provided on this Website relates to issues within the Company’s area of professionalism, the information contained on this Website is not a substitute for advice from a professional who is aware of the facts and circumstances of your individual situation. Nothing on this site, nor advice from our experts, shall constitute legal advice.